In a hugely connected world full of gurus, Chip and JoJo’s, multi-level marketing businesses and social media influencers, there are plenty of people that have the appearance of getting rich quickly. Every generation has had their different schemes and fads in gaining wealth. Truth be told, there are plenty of people who work very hard, do the right things, and make it to the top. But the stories of those who succeed are rare compared to those who just don’t quite put it all together.

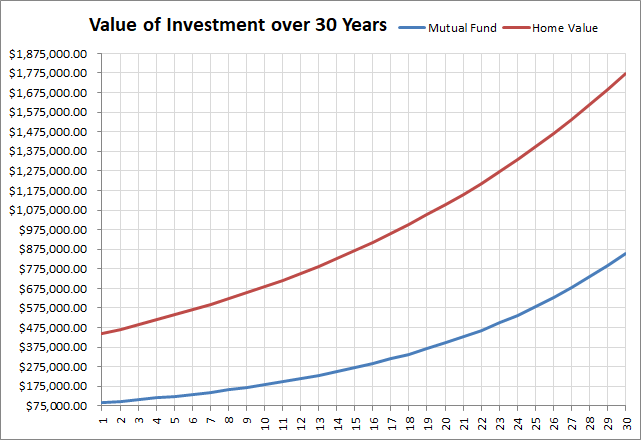

Real estate investing is no different. Often, late night infomercials tout the ease and simplicity of getting rich in real estate. Buying short sales and foreclosures, using “other people’s money”, investing in tax liens and “fix ‘n flip” programs make it seem like anyone can passively get rich. To be honest, I despise the get rich quick philosophy. In my opinion, it’s so much easier to make good, educated decisions over and over to both grow a significant nest egg, and mitigate risk over the duration of your investment. I say, “it just takes one”. It takes some upfront investment (just like a 401k, Roth, or Mutual Fund), but the results are simple.