There is still plenty of fear and unknown in the Northern Colorado real estate market and we aren't entirely sure how things will play out in the region post-COVID. What we do know is that there has been a constant demand for Northern Colorado homes in the last decade and we don't expect that demand to slow. Every homebuyer has fears of buying at a financially unsettled time. The best we can do is use data and projections to help us determine where the safest real estate in Northern Colorado actually is. This will help buyers feel more at ease knowing that their investment is safe and protected. Higher equity, lower debt is the first place to start.

In 2008/2009, the most impacted real estate in Northern Colorado were areas in which job loss, coupled with either adjusting or balooning payments on predatory loans created a perfect storm of short sales and foreclosures. That, coupled with eventual tightened lending caused a freefall in prices in the most vulnerable of areas. Even those who were able to keep their homes had their prices negatively impacted by these distressed sales.

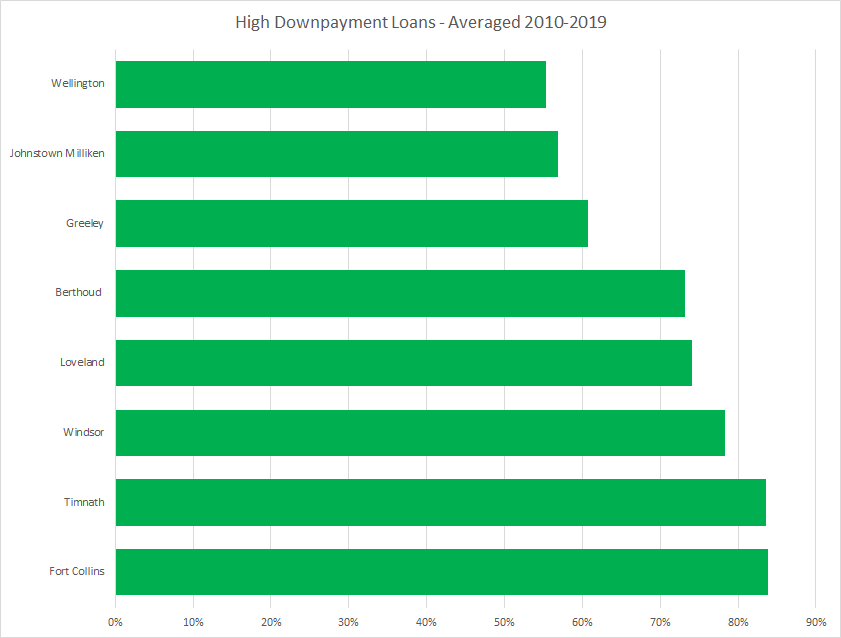

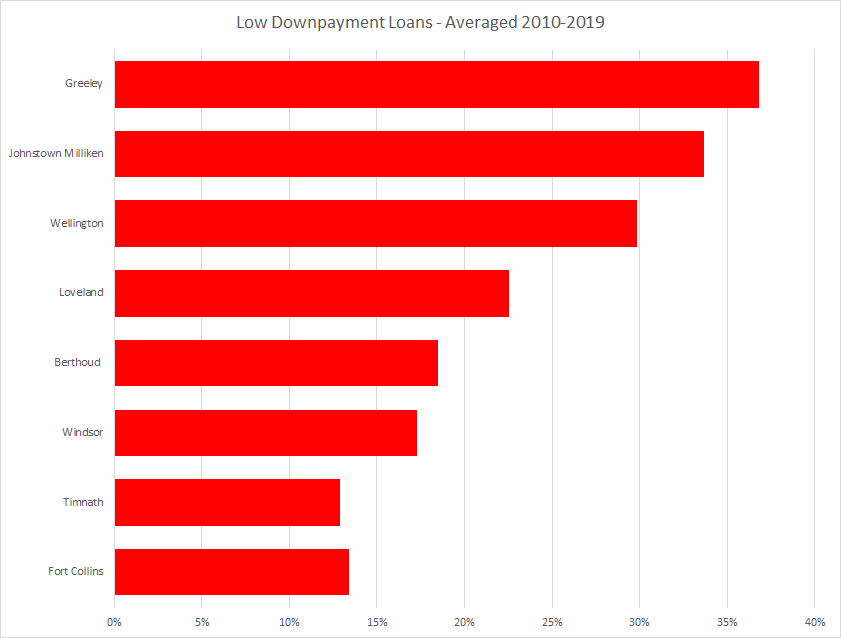

To gain a better perspective on which areas might be hardest hit, I did some digging to get an idea of the lending profile of homebuyers in each community in Northern Colorado. The results were illuminating.